")

Sometimes it can be really hard to find your way through the tax jungle. Legislators are therefore constantly trying to make things easier for people and entrepreneurs. That’s why the European Union invented the mini-one-stop store some time ago. This made it easier to pay taxes across borders, especially for companies that provide services. They had to pay taxes only if they exceeded certain individual thresholds of member states. In this case, taxes had to be paid in the country where the shipment started (so-called country of origin principle).

Now the EU has decided to extend this principle and created the EU One-Stop-Shop. As a result, these thresholds are now abolished and the country of destination principle (i.e. where the goods are shipped or the service is performed is where tax is paid) applies. Companies will now be able to register for this in their member state through the tax office and will then be able to pay tax on all transactions in which they are involved in a single tool. In the following article you will get all the important information you need to know about the new EU-OSS.

1. Basic informations

1.1 EU-One-Stop-Shop

As stated, as of 01.07.2021, the individual thresholds of the member states are no longer relevant, i.e. the sales will immediately be subject to VAT in the country of destination. In order to avoid that every company has to register in every member state where it provides services, the EU-OSS was created. It allows to pay the taxes to the tax office of one’s own member state, which then forwards them to the respective countries.

1.2 Registration

In order to use the new tool, you would need to register with the tax office in your member state or in the member state of identification (MSI). You must register in that calendar quarter BEFORE you plan to file your first return or in which you plan to perform your first services. (If you are already a member of the Mini-One-Stop-Shop (MOSS), you do not need to register separately).

1.3 Incurrence and correction of tax liability

The tax liability for your services arises when the service is rendered, NOT when your customers make payments. The declaration and payment of taxes must be made on the last day of the month following the declaration period. You must also submit declarations without sales (so-called zero declarations), otherwise you will not be able to use the tool in the future.

| Declaration period | Payment |

|---|---|

| January - March | 30. April |

| April - June | 31. July |

| July - September | 31. October |

| October - December | 31. January |

Of course, there is also the possibility of correction of the declaratio within 3 years from the day on which the original declaration should have been made. This must be done, for example, if goods are returned to you and you have to make a refund of the turnover). However, tax adjustments can only be offset against tax charges of the same member state. If this results in a negative tax amount, this can NOT be compensated by the OSS (pay-only system).

2. Deliveries within the EU

What are the requirements for an intra-Community mail order, which can therefore be processed via the EU OSS?

On the one hand, goods must be shipped from one member state to another member state (cross-border element) and to certain customers (such as non-entrepreneurs). Furthermore, you must be directly or indirectly involved in the shipment.

If you meet these requirements, you can process the following 4 types of transactions via the OSS without any problems.

- You sell from Austria to another member state

- You have a permanent establishment in a member state other than Austria and sell to another member state or also from the permanent establishment state to Austria

- You sell from Austria to the member state in which the permanent establishment is located

- Sales from your external warehouse to another member state.

Permanent establishments are treated as a separate company in the OSS, i.e. all sales originating from the permanent establishment must also be reported separately in FinanzOnline.

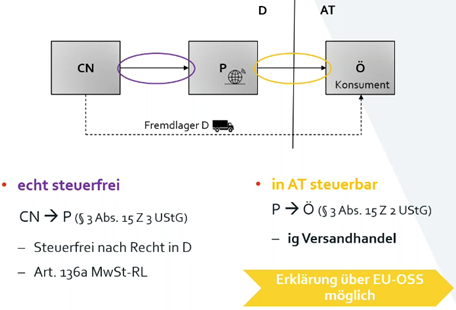

2.1 Deliveries within the EU via a platform (such as via Amazon)

If you decide to sell your goods via a platform, this platform is also treated as a separate tax debtor. You have to register it separately, or you have to mark the sales on FinanzOnline as being generated via an “electronic interface” (i.e. all sales generated via the platform have to be entered separately). In order to use a platform, you only need to use it for support. The platform is used for support whenever it is NOT ONLY used to process payments related to the delivery, the items are only listed on the website or it is only used to advertise your services.

Example:

The manufacturer of the goods is based in China, the “headquarters” of the platform (e.g. Amazon Germany) is in Germany, and the consumer (i.e. the end user) is residented in Austria. Legally, there are two separate deliveries here, even if the platform (or, if applicable, the entrepreneur behind it) never physically comes into contact with the goods.

The first delivery from the Chinese manufacturer to the German platform is tax-free, whereas the second delivery from Germany to Austria is taxable in Austria (destination principle) and can be handled via the OSS.

Illustration 1: Source: WKO Webinar EU OSS from 04.06.2021

3. Import mail order

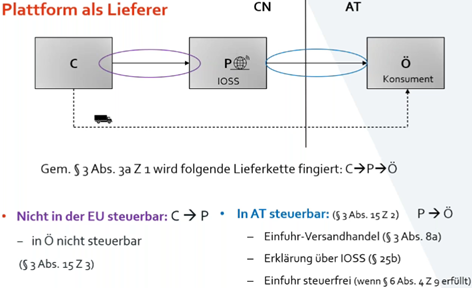

The OSS or in this case the IOSS (Import-One-Stop-Shop) can also be used by you if it is not about intra-community deliveries, but also if you import goods from a third country. An import occurs when goods from third countries are delivered into the EU territory. Unlike in the past, this delivery is now taxed from the first cent (not as before only from about 20�). In order for you to be able to process these sales via the IOSS, similar requirements must be met as for intra-Community mail order sales. Namely, the goods must be shipped from the third country to a member state and also the (European) entrepreneur must be directly or indirectly involved in the transport. In addition, the recipient of the delivery (final consumer) must be a consumer. Separate regulations exist for deliveries below 150�.

** 3.1 Import mail order via a platform** The tool can also be used for an import via a platform if the platform has its registered office in a third country. And the trader (i.e. you) has the registered office in a member state. Here, the platform must be opted into its own tax debtor in FinanzOnline too.

Example:

Initial situation is that the platform has its registered office in China and the end consumer in Austria. Again, only the supply between the platform and the end consumer is taxable if the above conditions are met.

Illustration 2: Source: WKO Webinar EU OSS from 04.06.2021